Go on, Take the Money and Run

This year has been one giant mess. It doesn’t appear it will be any different this week. We’ve got fires burning in California that are bigger than the entire state of Rhode Island and two Tropical storms racing into the Gulf of Mexico at the same time. This week’s post has three main sections. First, I review Equities. People getting smashed on short Tesla is the main article there. Then we move onto the Macro section. There’s a lot to digest there, but it’s the main chunk of the post this week. I cannot recommend the Macro MasterMind podcast enough. It was going to be the best of the week, but Tesla has been in the forefront a little more. I think the Mastermind series will help you move forward with investing for the future. Next, we hit the Credit section. I can’t recommend any of these articles more than the others. I found tremendous value in each of them. Finally, the Miscellaneous section has a great article on pensions and a long form historical piece on Public vs. Private markets.

For this week, I’m watching Tuesday’s New Home Sales numbers on the Economic front. The entire housing market is a hot bed right now. Home Depot (HD) and Lowe’s (LOW) reported excellent earnings last week. DR Horton (DHI) did as well. The price of lumber (LBc1) is up more than 100% year to date. For earnings, we’re still getting some laggards reporting Q2 earnings, but less than 10% of Russell 1000 names and 5% of S&P 500 names have yet to report. Some bigger names I’m interested in hearing from this week are Best Buy (BBY), Dick’s Sports (DKS), and the Dollar brothers, Dollar General (DG) & Dollar Tree (DLTR.O). I’m specifically following DKS though. With Foot Locker’s good report last week (see more on that below), I think DKS could surprise here as well and the SmartEstimate agrees (+17% EPS predicted). Along with the positive surprise the EPS has seen strong revisions higher and is in the 99th percentile in the Analyst Revisions Model as well. Looks like we’ve got a possible downside surprise as well. Ulta Beauty (ULTA.O) is showing a huge downside risk of -139.6% on EPS. EPS has seen an average revision of over 50% in the last thirty days. The stock was down over 6% last week. I’m also following the Fed’s Jackson Hole retreat and the Republican Convention starting virtually from Charlotte.

Before we get to the best content this week, I wanted to circle back to Foot Locker (FL), which I highlighted last week. With FT, we had a great example of the benefits of the Starmine SmartEstimate. Whether you’re a quant that just looks at the numbers or discretionary, these numbers can bring outliers to your attention. In Footlocker, we had a news story out a week or so before earnings, where the company updated guidance on their upcoming report. I think the reason they did this was that The Street was way negative on their forecasts, but the company thought they’d be around $0.66-0.70/share for non-GAAP headline numbers. The stock reacted with a 9% jump. Sixteen of the twenty-one brokers that cover the security updated their estimates over the next two days. Five brokers did not and there was a significant lag in the Mean taking the guidance into account. This is an important example of the Cluster exception in the Starmine SmartEstimate weights. A material change in the stock and not all brokers made adjustments. The stock traded off the jump back down near the levels before the pre-announcement. In two days before earnings, the three brokers highlighted in green finally updated their numbers and we saw the mean jump another 15%, but was still 21% below the SmartEstimate. The last two holdovers did not adjust and that kept the mean well below the expected value. The company outperformed even the guidance it had given and the stock jumped by 6% at the open, only to trade off the highs for the remainder of the day. I think this is a good example of why we pay attention to the SmartEstimates. When it’s greater than 2% away from the mean, it’s directionally correct about 70% of the time.

Best of the week:

We’re all aware of this story, but someone wrote it down. Now, when we talk about it in twenty years, we’ll be able to prove to people we’re not crazy. I’m surprised we didn’t see a little bit of a jump in Short interest after the split bumped the price up even more. We have seen a little bit of a bid to the implied volatility options, which tells me the shorts are using options to place bets rather than straight shorting. Below I’m using the S3 Partners add-on app in Eikon to track the shorts in between the exchange reports. Also looking at the longer term chart of the ATM 30 day Implied Vol chart. The final chart is the volatility surface on Aug 11th, pre-split announcement versus what it looked like at Friday’s close. Using the SURF chart, you can see the increase in implied volatility, but also that the downside skew has increased by about 30% while the upside is about the same. One final thing to note, Tesla (TSLA.O) closed on Friday at 2049.98, which is just about 50 pts or 2.4% away from 2100. Why is 2100 so magical? Well, with a 5 to 1 split on the calendar that number would put the post-split price at the mystical 420 level.

‘The Longest Unprofitable Short I’ve Ever Seen.’

Best of the rest:

Equities

This article continues on the Tesla train above. This article makes the argument for the fundamental overvaluation. I don’t think many would argue with the data or story in this article. However, stepping in front of this stock has shown to just rip your face off. Hopefully, the split will allow some more downside bets to be placed, before the bottom falls out of this stock.

Tesla: The Most Dangerous Stock for Fiduciaries

I’m a big fan of value investing. It was the first thing that got me interested in finance. In the midst of the Internet bubble of the late 90s, I switched from Marine Biology major to Finance, because a senior in my dorms was telling me about a paper he was working on picking stocks. In the end, it was a simple dividend discount model for value, but it got me hooked. Trading high flyers is fun, but diving into numbers and finding better ways to value firms is my favorite. In this article, Jack dives into Value versus Growth. He takes a different approach than the Russell indices do for defining value and growth and makes an argument that value might have been as bad as advertised.

Value Investing: An Examination of the 1,000 Largest Firms

This link is a two for one. Within the article is a short video interview with David Kelley, Chief Global Analyst at JP Morgan Asset Management, where he talks about what could stop this current run in US markets. Things like lack of pandemic response or higher rates and inflation in 2021. The article references some of the money moving into tech heavy ETFs as well as funds like GLD and corporate bond funds.

The next bubble: Passive investing in ETFs

This is a summary of a longer paper, but just the summary is something of interest. The authors of this paper used machine learning, specifically NLP, to delve deep into the the Refinitiv StreetEvents database of Earnings Call transcripts looking for tendencies when calls use certain phrases or have a tone to them. Short answer: they found a link between certain phrases and negative performance. These sort of NLP applications are the next level to the already used machine learning processing of the News headlines from the Refintiv Machine Readable News product.

Fascinating Research Alert: Earning Calls, Clichès, and Negative Abnormal Returns

Mike Green shared a chart on Friday afternoon showing the rise in wages for those who are still employed. Mike, who has been highlighting some of the problems with the rise of passive, brings up that inflows haven’t gone down because those of us still working hold the majority of 401K assets.

Macro

Fantastic conversation around Macro drivers. There’s so much content in this episode. Big discussions around the Dollar/Currencies, Gold, Bitcoin and the fiscal situations worldwide driving markets in those assets. Here a few of the biggest ideas that came out of this conversation:

Jeff Booth - “Removal of fiscal stimulus, short everything. There is a repricing event coming.”

Commodity rich countries like Russia & Kazakhstan are moving reserves into Gold.

India issuing sovereign debt that’s Gold backed

We’re moving to a multi/regional base currency world.

Companies are starting to put Bitcoin (BTC=) on their balance sheets instead of cash. (see MicroStrategy MSTR.O)

Macro Mastermind w/ Lyn Alden, Luke Gromen, & Jeff Booth - Listening time: 99 minutes

This story might be one of the reasons we saw some weakness in metals and maybe Bitcoin/Crypto of late. The Lira is getting beat up verus most major currencies. Local Turks are said to be scrambling into Gold and even Bitcoin as ways to fight off inflation.

Turkey Residents Panicking Over Massive Inflation

Roger Hirst discusses Dollar with Julian Brigden of MI2 Partners and Macro Insiders. Is this recent downside move in the DXY more of a Dollar story or Euro story? Julian noted that collapsing US yields are creating less of an attraction for Developed Market investors.

The US Dollar Bear Market? | The Big Conversation | Refinitiv - Watch time: 34 minutes

This report from FTSE Russell echoes some of what Roger and Julian discussed in the video above. The article also shows some of the help the falling USD has given to the emerging market equities and to Small-cap US stocks. This chart below shows the recent correlation between the Dollar and relative performance of the Russell large cap (.RUI) to the small-cap (.RUT). The report claims there’s strong positive correlation between USD and relative large-cap to small-cap performance. In their chart (below), it does show some linkage in the last year or so. However, if you extend the chart to look at the last 10 years, it’s not traditionally that strong.

The ripple effects of the falling US dollar

Unless you paid zero attention to financial news last week, you saw that Berkshire Hathaway took some of its massive cash position and bought shares of gold miner, Barrick Gold (ABX.TO/GOLD). Jesse Felder highlights that the purchase by Mr. Buffett is not the first time he’s dipped into the metals trade.

Why Warren Buffett Is Buying Precious Metals (Again)

Credit

Here is some more from JP Morgan Asset Management. Steven Learn, US CIO for Global Fixed Income, Currency & Commodities, and Rick Figuly, Head of Core Strategy argue for active investing in bonds. Steve mentions the price dislocation in corporate bonds in March that passive was unable to take advantage of. Rick highlights some buying of bonds that haven’t been in the Fed’s bond buying program. They also reference rates staying low for some time, but not moving to negative.

Fixed income investing in a low rate world - Listening time: 30 minutes

Nice summary from Guggenheim on the credit sector. The report reviews a lot of data on performance, spreads, and curves in various high yield sectors.

High-Yield and Bank Loan Outlook - Third Quarter 2020

Great article from the NY Fed’s Research and Statistics group. They highlight the actions taken by the Fed’s Open Market Committee and how that relates to past actions taken in 1939, 1958, and 1970. Summing up the article the author notes that while the size and speed of the recent program were unprecedented, the interaction itself was not unique. Finally, they think “relying on the Fed on those rare occasions when markets are in extremis has not materially exacerbated moral hazard.”

Market Function Purchases by the Federal Reserve

Once you find the bonds you want to purchase, how you purchase them continues to change. Electronic trading took a bit of a hit during the start of the pandemic. Things were moving too fast and many are saying that real time pricing suffered. That doesn’t mean that electronification of this market is stopping. Many players think this might provide some great info on how to improve the system. The human relationships are imperative for dealer markets, but new technologies will help lower costs and gain efficiencies.

The Buy Side’s Hunt for Bond Liquidity

Miscellaneous

Consolidation is the name of the game for governments. It’s a great way to save on services. Think about the benefits of things like regional high schools where towns share resources for principals, sports, and educational resources. Well, Canada did this for their pension plans and the article discusses the benefits for the U.S. to do the same. There are thousands of small and mid-sized public pensions in the U.S. and combining them into a “sweet spot” of roughly $50-250B in AUM might be better off.

America’s Public Pension Challenges Can Be Fixed. Canada Is Proof.

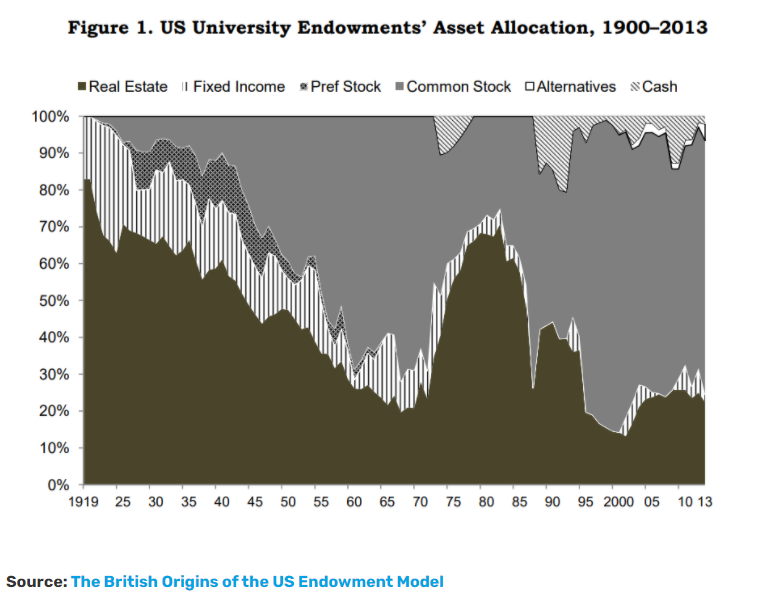

If you’re interested in longer form writing, Jamie Catherwood covers a ton of history on Public and Private market investing. Where pensions and the role of the individual have played into this over time. Jamie always does an amazing job of tying current events and history together and this week’s post was amazing. I loved his opening chart. Look at the role Real Estate played for university endowments historically.

The Public And Private Markets

Comments

Post a Comment