Let's Make a Deal

Last week was dominated by COVID news. The President testing positive was the biggest, but also the NFL had to postpone two games and New York City had to shut down schools in nine districts due to an outbreak. The Fed expanded its buyback and capped dividends restrictions for banks. It also approved the Morgan Stanley acquisition of E*Trade. Palantir (PLTR) & Asana (ASAN.K) were two of the most popular new traders last week. The direct listings were just a small piece of the busy week, which we'll highlight below.

The Charles Schwab - TD Ameritrade merger will finally go through this week. Beyond Meat (BYND.O) hits Wal-Mart stores this week. This should help boost Q4 sales. Nvidia (NVDA.O) holds an analyst day later today. FED chairman, Jerome Powell, speaks at the National Association for Business Economics Annual Meeting on Tuesday. We have the VP Debate on Wednesday. Let’s be honest though everyone is watching the President’s health and for a possible stimulus package.

Earnings’ Watch

Our three names to watch from last week didn’t do as the prior week.

- United Natural Foods (UNFI.K) had a very good quarter with a beat and raise, so the Starmine expected surprise nailed it. However, their CEO announced his retirement and I’m guessing investors were fond of him. The stock got banged for 8% after the report and ended the week even lower, down 14%.

- Bed Bath and Beyond (BBBY.O) had a 61% predicted surprise and a 16% expected move going into earnings and they did not disappoint in any way. Analysts expected a -$0.23 earnings and BBBY.O came through with $0.50. They opened up 28% on Friday and finished up ~43%.

- Micron (MU) was expecting a 6 cents or 2% miss, but the company beat by 8 cents or 3%. Opposite to what happened with UNFI.K the stock moved lower after the positive report. Opening the next day down 5% and ending the week down 8%.

- Delta Airlines (DAL), which reports on Thursday, shows a predicted miss of 5% and a couple of 5 star analysts off considerably from the mean. The EPS mean estimate is down 7.5% over the last 30 days, so it’s got that trend that we look for. The Implied Vol is a little elevated, but just 10% above the trailing 50 days on the 30day. The weekly options are pricing in a roughly 7% move. **I had this date wrong and now the numbers look much different.

- Dominos (DPZ), which also reports on Thursday, is not really showing me anything in the numbers, but I still have a feeling that they come in better than analyst estimates, but will it be enough. Predicted surprise is 1.7%, so that’s not much. Momentum in the EPS revisions stalled last week, so that metric doesn’t look good either. ATM Implied Vol is elevated, which is a norm for this company during earnings season. This stock is priced for perfection and trading at all-time highs, so the risk is to the downside here. If they do miss, look out below.

Best of the Week:

After hearing the podcast above, I went back to look at the Refinitiv ECM review for the US. It looks like Goldman Sach is leading the underwriting business. Looking at the six categories below, GS leads in four and is second in the other two. The top four banks, which consist of GS, Morgan Stanley, JP Morgan, and BofA Securities, really stand out above the fifth ranked bookrunner for the first nine months of deal value.

Refinitiv Global Equity Capital Markets Review

SPACs have become so popular that we now have an ETF for it. The ETF isn’t perfect if you want to track SPAC performance, but you know someone was going to try to capitalize off this trend. 80% of the holdings are made up of companies that have been already taken over by the investment companies, the other 20% is pre-merger investment companies.

A SPAC ETF Makes Its Debut Today. Here Is What You Need to Know.

This article explains some of the details around SPACs. What they are, how they work, and what the benefits and risks are for investors.

Blank-Check Companies: Be Careful

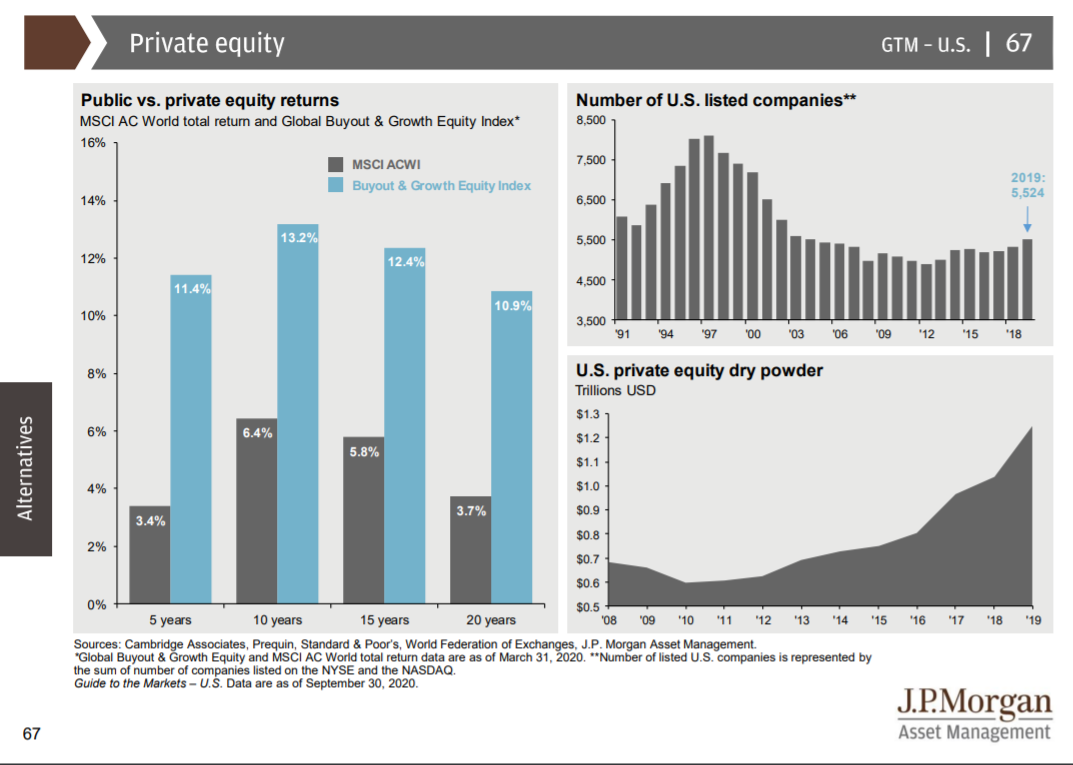

This is a plethora of charts. Seventy-six pages to be exact. This chart book covers nearly everything. I had a tough time picking just one chart to share, but this one continues on the topic from the IPO podcast above.

JP Morgan Asset Management - Guide to Markets

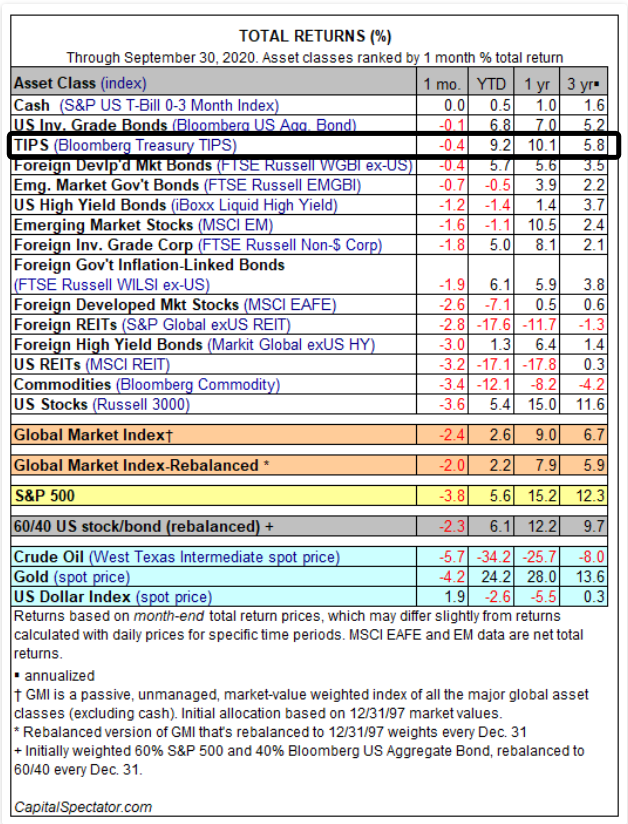

You’ve most likely seen something like this now, but I love this basic table showing global asset class returns for US investors. What stood out to me looking this over was the relative performance of TIPS.

Major Asset Classes | September 2020 | Performance Review

Last week, I was talking with our new associates about the impact of retail trading and the unabashed enthusiasm for stock these days. He asked if this is the craziest it’s been. My answer was no way. I then explained that I was his age (early 20s) through the Dot-Com bubble and how that period was just completely insane. The one thing that’s more aggressive these days is the use of options, which I’ve shared before. Nick’s piece this week put some numbers to my anecdotal thoughts. A continued move higher with an ever increasing amount of SPACs into companies that make no money and trade on completely useless metrics might change that, but for now we still have room to run on ridiculousness.

No, This Isn’t a Repeat of the Dot-Com Bubble

You’ve probably sensed that I cannot go too long without referring back to volatility. This week Meb Faber talked with Cem Karsan, aka Jam Croissant on Twitter. Cem started Aegea Capital to capitalize on long vol strategies around the inefficiencies in 30 day vol. Of course they eventually got into the election and how Cem sees the markets pricing in the risk of volatility. My favorite point comes when Meb asks Cem what the structural inefficiencies are. The six minutes from the 16:40 mark can be the only part you listen to from the episode and it would be great, but there’s so much more value here.

Cem Karsan, Aegea Capital - 30 Day Vol Tends To Be Overbid And You Have Extended Supply In The Back Of The Curve Historically - Listening time: 56 minutes

Macro

This was a good discussion around the Dollar, Gold & Silver and how those are moving in conjunction with the US Markets. Jim is a seasoned trader and talks about how he’s thinking about the near term volatility around the election as well. Like a few others of late, Jim thinks the volatility worries are most likely overblown and things will not be as bad as the market is predicting with the elevated VIX futures.The dollar is the ‘dog,’ and stocks are the ‘tail’: Jim Iuorio - Listening time: 29 minutes

This was on ZeroHedge on Monday, but it’s really mostly from over a week ago. I’m sure you’ve seen this chart from the WSJ article, but it stood with me all week. I’ve seen my Facebook groups filled with people selling older bicycles at prices that are insane. If the bike rolls, you can get $100 for it. This ZH post has some great charts around inflation and if you click on the Nordea link that goes to Andreas Steno Larsen’s report, there’s even more. My point in sharing this is that I believe we’re going to get some serious inflation, but it may not be the inflation the CPI tracks or we expect.

"Inflation Is Already Here": The Fed May Have A Major Problem On Its Hands

Every week I receive an email, phone call, or old fashioned mailer from realtors looking to help me sell my home. The talk around housing has come back. Home Depot, Lowes, and the rest of the home improvement segment has been killing it. I’m surprised in the chart we saw above that there were not any home building/improvement related items. The Capital Spectator asks if the combination of new and existing home sales can drive the economy. Think about all the space city dwellers need to fill when they move to the suburbs. If this trend of moving out of cities gets legs, there are a lot of secondary purchases that need to be made.

Will Housing Save The US Economy?

Energy

One of the reasons, I try to get to so many different sources each week is to find trends or people coming from different points of view that come to the same conclusion or argue against one another. This week Jesse Felder is making a point that energy is getting pummeled and treated like the red-headed step child. Maybe, it’s time to consider energy for a trade. Sentiment Trader also published some stats around the magnitude of how bad energy stocks have been lately. Oil guru, Art Berman, joined the MacroVoices podcast this week. Art is looking at the big dip in demand and the shrinking rig count. The big point I took from Art is that as demand continues to lag, production will slowly go more dormant. Then when demand returns, it takes six months to a year for the wells to start producing again. That means oil could rip in the meantime. There’s so much more around here in the charts, but it’s best if you listen to Erik and Art talk about it, especially if you have anything related to oil in your portfolio.It’s Time To Get Greedy In The Energy Sector, Part Deux

Art Berman Macro Voices Charts

Research

As you might guess from the headline, this author reveals that Robinhood might not be the pure punters that their reputationOpinion: Here’s the shocking truth about Robinhood investors vs. Wall Street stock pros

Professor Nicole Boyson joins Toby to discuss how activism affects returns of the target companies. She breaks down the different types of activist, transactional vs. those are more long term, and how those differences have played out. Her paper was published a few years ago and might be worth looking over if you trade arb names.

Activist Hedge: Nicole Boyson on activism in academia - Listening time: 50 minutes

Thanks for reading,

Michael

Comments

Post a Comment