Guess Who's Back

“Now this looks like a job for me

So everybody just follow me

'Cause we need a little controversy

'Cause it feels so empty without me”

For this week, I’m interested to see if Value can gain some momentum on last week's events or if this is just a head fake. As we’ll see in the Earnings’ watch, retail will be a big story this week. With the US pulling out of many of its trade deals and in this case specifically the TPP, we saw the largest trade deal excluding the US announced over the weekend. The Regional Comprehensive Economic Partnership (RCEP) is made up of South Korea, China, Japan, Australia, New Zealand and 10 smaller Southeast Asian countries.

Earnings’ Watch

Looking back at last week, earnings were quite eventful. Disney (DIS) probably generated the most buzz. The stock rose as much as 6% after they announced their 73M+ paid subs for Disney+. FYI, they were targeting 60-90M by 2024! The company’s other division struggle, but investors and traders seems more focused on the future of digital. Cisco (CSCO.O) also did well after posting a less than expected drop in growth. Top and bottom line numbers were down about 10%, but the Street was expecting more.For the names I spoke about last week:

- Dillards (DDS) beat by even more than expected reporting an $0.08/share gain vs. the mean of -$0.86/share. The stock opened up 8.5% and closed the day just off the highs up 5.8%.

- Callaway Golf (ELY) put down the fairway on their report, but things seem to have hit a sprinkler head. The company beat on both EPS (60%) and Revenue (5%), but lack of guidance and some concerns over the TopGolf acquisition seemed to have weighed on the stock. It opened down slightly -0.8%, but traded down 8.3% and finished the week down 10% from the pre-earnings close.

- NOVAVAX (NVAX.O) had a huge miss on both top and bottom line numbers. Opposite of Dillards, NOVAVAX flipped from positive EPS expectations to a huge loss of $3.21/share. On top of the bad earnings’ news they also announced a $500M stock offering. The stock traded up as much as 12% the day of their after market close report. After the miss, the stock opened down 5.5%, traded down as much as 15%. The interesting thing here is after its midday Tuesday lows, it rebounded. From the Tuesday lows, the stock rallied 25% to close the week up 7% post earnings report. I only saw some positive vaccine news out of India for the company as a possible late week catalyst.

- L Brands (LB) has an odd detailed estimate profile for this quarter. 22 of 23 analysts covering are included in the Starmine SmartEstimate, but 7 have less than a 2% weight. The majority of the weighting (33%) is three of the four 5-star analysts covering the stock. That’s also where the battle will play out. Two of them, Morgan Stanley and Robert Baird, are well below the mean. Robert Baird’s estimate is from August and one of the oldest. On the high side, MKM Partners and JP Morgan are both more than 100% higher than the mean. JP Morgan all the way up at $0.55/share on an $0.08/share mean. The company surprised last quarter by 160%. The quarter before was the first time they did not beat the Street since Q3 2007, or 49 reporting periods. I’m thinking the Predicted Surprise has a good shot of being directionally correct. The short term weekly options have an even more elevated implied volatility compared to the ATM 30D and there is a bunch of open interest on the call side. The December expiry deep out of the money calls have a caught bid to them.

- Target (TGT) had a small cluster of analysts update their EPS numbers in the last two weeks. Most of those coming on the Ulta Beauty news. There’s one 5-star analyst, Jefferies and their number is right one the mean. The company has beat the Street for 7 straight releases and 8 of the last 10. Nothing in the options on this one look too far off normal. The implied move for the week is +10%, which looks on the high side. The stock has only moved that much in a week 7 times in the last 2 years. That’s roughly a 2 sigma event.

- Lowe’s Companies (LOW) has 30 analysts covering it. 27 are included in the Q3 EPS mean, but, like TGT, only 10 are used when calculating the Starmine SmartEstimate. The Predicted Surprise for Wednesday’s report is about 6% to the up side. The SmartEstimate has increased by 6% over the last 7 days and 9.8% over the last 30. Last week, JP Morgan’s five star analyst, Chris Horvers, upped his estimate to $2.37 which is 20% above the mean. Look for some updates in estimates on Monday and Tuesday, but I still think this stock has a good chance to outperform this week. The company has beat analyst estimates the last five quarters and 9 of the last 10.

Best of the Week:

If you’re not following Jamie Catherwood’s work, you’re missing out on some fantastic content. Jamie has been writing about financial markets history for a bit now, and the stuff he finds is absolutely amazing. In this Tweet, Jamie highlights some writing on the 1886 Guinness IPO. Some of the writing here is just great. In the thread, Jamie does some additional highlighting and commentary. My favorite part is given some extra attention from Jamie, “ "When the mood is upon them, the public will not believe in fraud, any more than thirsty soldiers will believe in poisoned water. They see a few men making profits, and the warning that they will be made out of the latest holders is preached to deafened ears."

Excellent insight into human nature via a description of the Guinness IPO in 1886, and investor mania.

Best of the Rest:

Value’s Comeback?

One of my FinTwit mates published this chart on daily returns of Momentum and Value from Monday’s epic market following the Pfizer vaccine news. One of the comment notes that according to Goldman Sachs, "the ~16% reversal in our l/s S&P 500 Momentum factor (GSMEFMOM) was the largest one-day decline in the factor's history since 1980 - and it wasn't even close (-10% in April 2009 was the prior)."Historic Factor Moves

The rebound we saw last week helps Value’s drastic underperformance to Growth. In this post, we see the current one year returns vs. a historical data set. As the author points out, it’s not unprecedented, but it is unusual. The article also has a second chart showing this for small cap names.

How Unusual Is The Current Drought For The Value Factor?

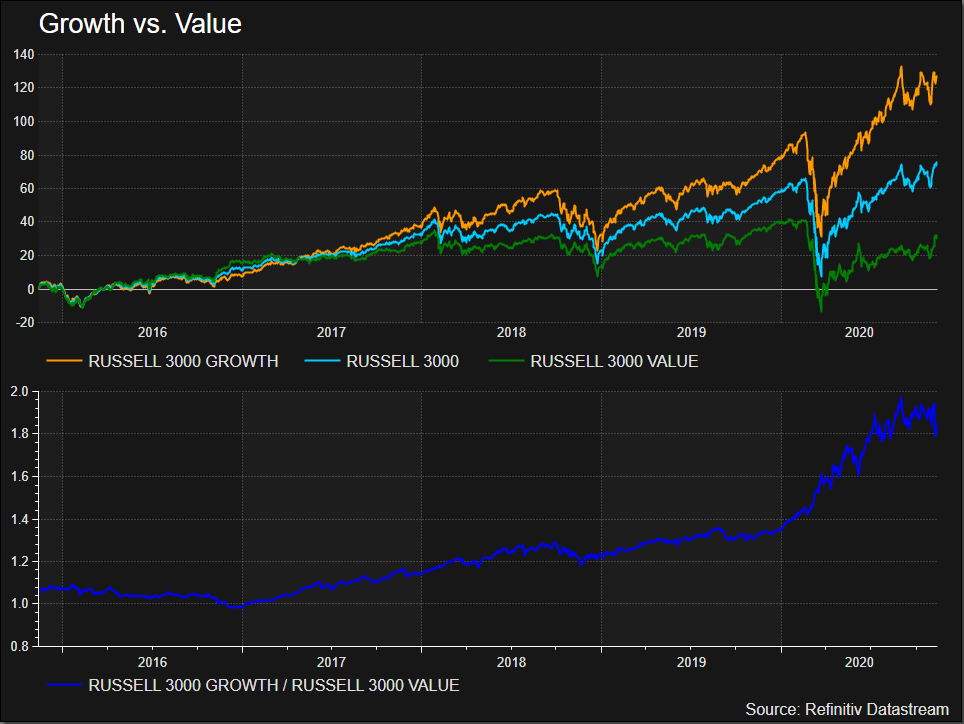

Rob talks with ‘Institutional Investor’ about the snap back in Value last week. Value has been getting trounced by Growth. The article mentions that it’s the worst since 1931 thru early September, but as Arnott points out finding the catalyst that will spark the turnaround is fun, but may never actually be known. Ed Moya says in the article that this is probably more of a blip than the start of an actual comeback. I took a look at the Russell 3000 Growth and Value over the last five years (picked at random), you can see growth outperform in 2018 then comeback, the virus slide in March brought both lower, but Growth still outperformed and then really put Value in the rearview in the next few months. However, since about August the returns have started to level out with Value making a few attempts at a run. Regardless, the daily returns were quite phenomenal, as we saw above. The daily percentage returns show it was the largest underperformance for growth by quite a large amount.

Rob Arnott Sees Value Recovery Taking Root After Worst Meltdown Since 1931

Horses for Courses

I’ve covered how staggering a reversal it was for Value last week. When I saw this post, I wasn’t really surprised but I was still amazed at how much some of the names were down with momentous returns on Monday.

One Look At Monday’s Massive Rotation

Matt Peterson is the managing partner of his own investment firm, Peterson Capital Management. Matt joined Toby on The Acquirers Podcast to discuss his unique approach to value. Matt's approach is unlike anything I’ve ever heard before. He uses options, specifically selling puts to get into deep value equity positions.

Structured Value: Matt Peterson on options and value - Listening time: 56 minutes

Fixed Income & Rates

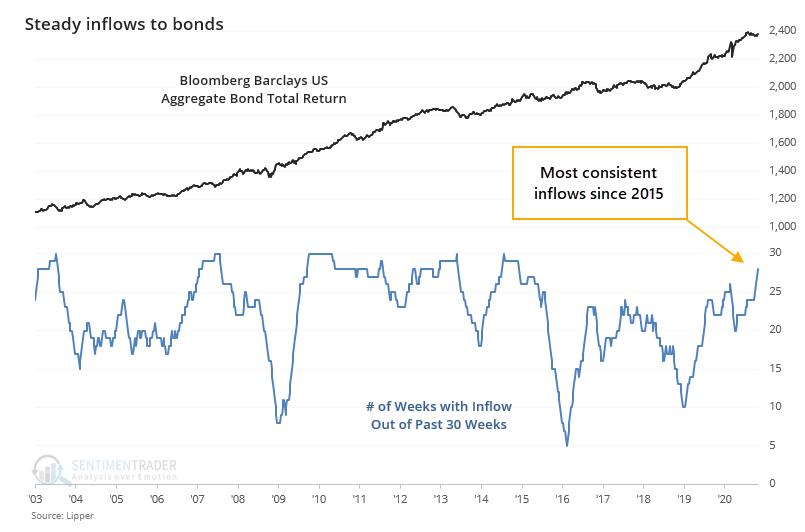

Jason uses some Refinitiv data from the Lipper fund flows to show the steady inflows into bonds.Bond investors did this for only the 2nd time in 6 months

This is a fabulous conversation Dean has with Josh. Much of it is beyond my experience with these markets. I had to listen to this three times to really get a deep understanding of what they were talking about. Granted I was also watching football, so maybe it wasn’t really all that difficult. Josh explains how the post GFC regulation and other incentives left the US Treasury market exposed. Of course, they also talk about the near collapse of the Treasury Market in

March. There’s so much more around interest rate options and volatility here too. This was a close runner up for the ‘Best of the Week’.

Josh Younger, Head of US Interest Rate Derivative Strategy, JP Morgan - Listening time: 58 minutes

More Equities

Finding the right benchmark to grade a trade was sometimes a tense discussion on the trading desk. Whether it was on the sellside talking with my buyside clients or the buyside arguing with the PM, there’s a lot that goes into how you grade a trade. Honestly, I felt the other side always had 20/20 hindsight vision. The team at Pragma believes they have found an answer to better measure execution quality. This article is a good summary of the problem, but I recommend downloading the research report.A New Benchmark to Help Traders Improve Execution Quality Measurement

Measuring Execution Quality – Finding the Signal in the Noise (November 2020)

Identifying Resilient Companies in a Financial Crisis

Saw this chart from Susquehanna Tweeted out last week. There is a good discussion on both Cem’s reTweet and the original. The Fed actually wrote a research paper on this back in the summer, and someone links to it in the post.

S&P 500 Overnight vs Open Market Returns

The Market Ear team sent out a sentiment themed newsletter edition early this morning, and it had a bunch of excellent charts. There were a bunch of indicators in there that were common, but this is one that I’ve never seen before, so I thought I’d share. I cannot recommend their daily charts newsletter more.

ESG

This post is very negative on Tesla, but the staggering numbers of CapEx budget Volkswagen and other EV producers are huge compared to what Tesla is planning. If you want to understand what’s going on in the EV space, this is a good article. I also took to the Industry app in Eikon to look at the last fiscal year CapEx and the IBES estimates for the next three years. Tesla has less Capex than internal combustion car markers like Suzuki, Kia, Subaru all who have market caps less than 1/10th that of Tesla.

Remember a few months back when Kodak surprised everyone with a new government contract and we found out that insiders had miraculous timing on stock and option buying. Well, we possibly had another one of those suspiciously convenient yet legal transactions on Pfizer’s vaccine news. The company’s CEO sold about $5.6 Million worth of stock and their Chief Corporate Affairs Officer, basically PR, sold about $1.8 Million as well. Both transactions were apparently legal under a 10b5-1 trading plan. The company commented on the CEO’s transaction. "Through our stock plan administrator, Dr. Bourla authorized the sale of these shares on August 19, 2020, provided the stock was at least at a certain price," a Pfizer spokesperson told Business Insider. Those sales moved PFE from an already low 35 on the Starmine Insider Filings model down to a 26. You can see the last few months charted for PFE.

Pfizer's CEO cashed out 60% of his stock on the same day the company unveiled the results of its COVID-19 vaccine trial

Capital Markets

Much of the news surrounding the halting of the gigantic IPO of Ant Group in Asia last week claims political motives. Li Nan, Professor of Finance and Economics at Shanghai Jiao Tong University, joined Jeremy and Liqian Ren to give her views on Ant’s business and how it might truly be predatory to Chinese individuals and small businesses. Also, Ant benefits from the revenues but will leave smaller Chinese banks holding the bag on defaults. This is a good discussion for those that invest in China, especially in Ant’s partners and competitors.Behind the Market: Li Nan on Ant Group - Listening time: 30 minutes

China's Xi Jinping personally halted Ant's record-breaking $37 billion IPO after boss Jack Ma snubbed government leaders, report says

Inside The End-Of-Year IPO Rush

Comments

Post a Comment