Wall of Worry

Most equity markets had a down week. This was the second red week in a row, which has only happened two times in the last year. The last time we saw three consecutive down weeks for US markets was a year ago this week. There was a lot of red out there globally too. Hong Kong and China were some of the worst performing. China, and in turn Hong Kong, was down again on regulatory worries out of Macau. Another big story last week was the developments with China Evergrande Group’s credit issues. Below, I share a couple of links that cover this, plus a few screenshots from Refinitiv’s Eikon desktop product. Another thing I’ve been noticing more and more with the equity markets, the wall of worry is getting steeper and steeper. This week something like half a dozen tier one banks have made calls for a selloff. We also see below in the BofA Fund Manager survey that a lot of managers are not expecting a stronger economy. This has led to some pretty expensive downside protection for the major global indices.

Earnings Watch

We don’t really have a ton on the calendar right now, but there are a few names of interest to watch. Last week, Oracle performed well on their quarterly numbers, but the stock got smashed. Coming up this week, the big names are Adobe, Nike, Costco, FedEx and my favorite cereal maker, General Mills. Home builders Lennar and KB Home should provide some insight on the crazy housing market. A smaller name to keep an eye is Stitch Fix, which shows a 12% Predicted Surprise.

Equity Capital Markets (via Refinitiv’s IFR)

Last week saw some serious activity and it doesn’t look like things will slow down any this week. Last week’s IPO had some decent performance too. Six of the IPOs priced above range, three were upsized, and none finished below their offer price. Top performers were DICE Therapeutics, Dutch Bros, and ForgeRock.This week we’re expecting another 14 IPOs in the US looking to raise about $5.6B. Freshworks @ $912M and Toast @ $717M are the two largest scheduled for next week.

Best of the Week

SALT NY was a three day event last week and the conference had an impressive lineup of speakers from many different backgrounds. This session was a who’s who of hedge fund stars. This session was moderated by Barry Ritholtz. They discussed the state of the industry, performance, risk, entrepreneurship, hiring, and a bunch of other topics. You may not recognize why Ilana Weinstein is on this panel, but she’s well known in the hedge fund industry and places many of the biggest PMs in their jobs. There are so many gold nuggets in this conversation. I really cannot recommend watching it enough. Especially, if you’re interested in the business of hedge funds.The Hedge Fund Comeback: Steve Cohen, Ilana Weinstein, Dmitry Balyasny & Mike Rockefeller - Watch time: 44 minutes

Best of the Rest

A $200B company that owns about 2% of all property in China is about to default, if the Chinese government doesn’t step in. Sharing this version, because I think Steve is a great resource for macro. He covers a lot of topics in just over 20 minutes. I’ve also included the Real Vision Daily Briefing, where Jim Bianco discusses this with a few more highlights and how this might impact the rest of the world. Looking at the company in the Starmine Combined Credit Risk view, I can see it’s been trending lower for a while, but started showing some more serious issues in June. The stock had already started to sell off by then. It was off roughly 26% from its 2021 high. Since the credit issues started to really show, the equity is off another 82%. My colleague helped me with looking at the company’s credit curve over the last couple of months using Refintiv Eikon’s Yield Map app. I also looked at the spreads, not pictured below because they are astronomical. I saw over the weekend that they are paying off some debt with actual real estate holdings. Keep an eye on this, it might set off some other problems, but Jim mentioned that he thinks it’s all been priced in.A Massive Meltdown of China's Real Estate Market Could Trigger Global Liquidity Crisis - watch time: 23 minutes

Does Evergrande Pose Broader Market Threats Outside China? - Listening time: 33 minutes

Crazy trading story from the year 2000

The 4th Longest Momentum Streak Since 1928 Just Ended

This one might be a bit controversial, but Aswath is a valuation expert and is coming back at ESG. In a Tweet thread last week, he disparaged the investing style. He feels it is difficult to measure goodness because we have different value systems.

'Dean of Valuation' Aswath Damodaran still cannot find any going points with ESG

One for the Road

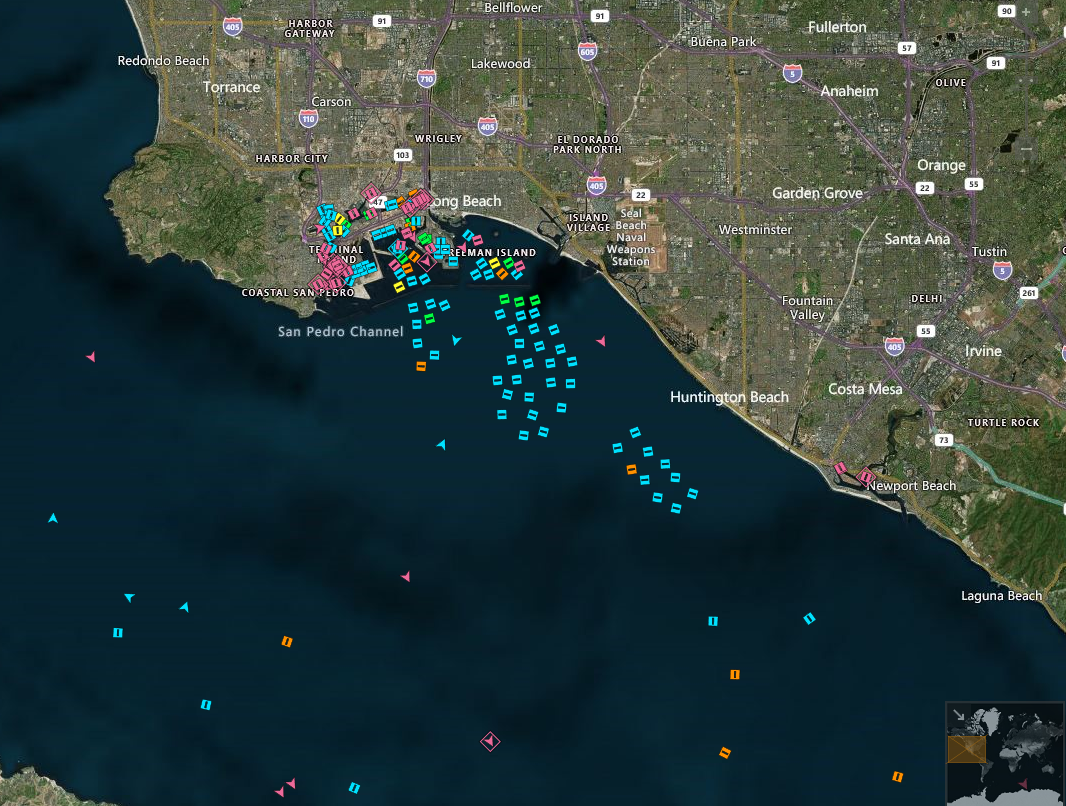

Just a friendly reminder that shipping is still all messed up. If you haven’t thought about Christmas, yes it’s less than 100 days away, you might want to start, like now. I mean the delays coming into LA from Asia can be more than a week. There are delays at every point of the process.A tangled supply chain means shipping delays. Do your holiday shopping now

Record 60 cargo ships wait to unload at busiest U.S. port complex

Thanks for reading. Have an amazing week.

Michael

Comments

Post a Comment