This week some trends continue and some look to have taken a pause. In this week’s post, I’ll take a look at some of the data coming out of the quarter. It was a bad quarter for some assets and a really swell one for others. Yes, I just used the word swell. Sorry, but I was looking at classic cars with my dad over the weekend. The art of picking a title is hard, but this week comes via a song from one of my favorite bands. The hard part is then trying to find a picture that's ok to share. Below I'll touch on the BOJ trying to defend the Yen. I think they might be Digging the Grave here. JGBs, and pretty much most of the government bond market, are selling off. The curves are facing inversion and we may continue to see the Fed hiking. We might be up for a challenge for the remainder of 2022.

This week I’ve got a ton of charts that I looked through. One thing that I completely missed, which a colleague alerted me to, was that my Yen performance was inverted. Whoops! Instead of the normal weekly numbers, I zoomed out a bit and looked at the Q1 numbers, which like always, sent me down a rabbit hole. My major asset chart below shows the weakness in equities, the strength in Commodities. I realized right as I’m wrapping this up that I haven’t included anything here in the Fixed Income space. I’ll have to make that change next time.

As mentioned above, commodities had an exceptional quarter. The S&P GSCI index had it’s second best quarter in almost 50 years and its best since 1990. I picked up a couple of posts from the S&P DJ Index team below, but most of the insight is in the charts. You can see in the second chart that almost every single constituent of the GSCI was up in the quarter. Cattle was the weakest performer and most of energy was up huge. S&P GSCI posted its best quarterly return in decades

Commodities Continued to March Higher Last Month

Speaking of Energy, President Biden decided that he’s going to release 180 million barrels over the next 6 months. It’s going to be done at 1 million barrels per day. This isn’t too much of a worry, right now, as the reserves have more than 600 million barrels. My opinion is this is a desperate attempt to appease the voters. Regardless of my political leanings, I hate this decision. It’s something that is trying to fix some terrible decisions made to go overboard with the ESG regulations on oil and gas. I decided to take a look at the impact on equities of late and see if things have gotten over extended in this space. What is the SPR, the emergency oil stash Biden is tapping?

The jump in oil & gas prices has had an impact on the Energy sector in equities. Here’s a look at the Russell 3000 sector performance this year. Energy is killing it.

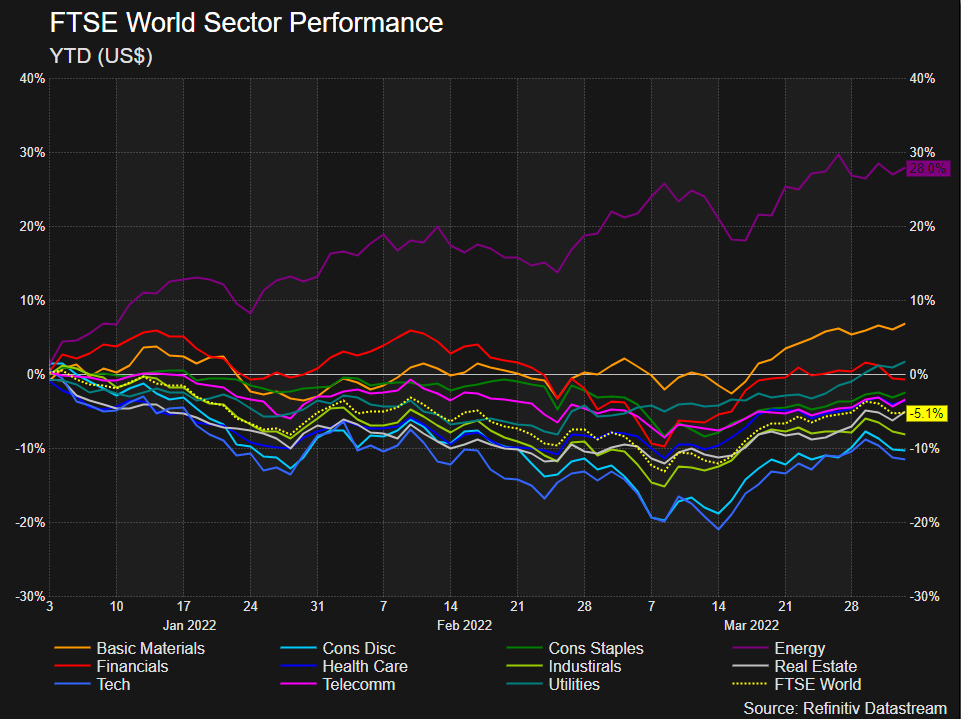

Is it just the US? Nope! While the sector’s outperformance in the FTSE World isn’t as strong as in the US, it’s still pretty strong.

Has this strong performance pushed the sector into an overbought position? Maybe short term, but take a look at the last ten years. Energy just squeaked into positive territory in the US and is still negative globally. JP Morgan’s Energy Strategy team agrees. Here’s a statement from one of their reports this week (bold emphasis is my own):

“We view today’s announcement of the largest SPR release in US history as the clearest indication yet that the future availability of production capacity is at risk owing to limited Shale and OPEC+ spare capacity coupled with prevailing strong demand. Importantly, it should be supportive of the back-end of the forward curve as the US Administration reveals a clear determination to help mitigate recessionary risks to demand arising from future spikes in oil prices. Net, net we expect a material positive re-coupling of energy equities to oil with today’s performance marking an important inflection point for the asset class (XOP up 1%; WTI down 4%as we write). Moreover, the sector should outperform even during periods of heightened volatility and a negative skew to the front end oil price.”

The last chart below is a look at the Tech and Energy sectors as a percentage of the total index. Even with Energy's recent run, you can see that just takes it from completely pathetic to very low. Tech still drives most developed indices.

This chart from Goldman highlights why equities might still be a better value for asset allocators than bonds. It also shows something I’ve been talking about for a bit. Certain EM markets might be a screaming buy. I’m looking at you Brazil, Mexico, India. Other commodity driven countries could benefit here too.Why Equities are Not Crashing

The Yen has been taking a beating. The Bank of Japan (BOJ) started to defend its currency by buying bonds. A move of this magnitude is rare, but not unheard of. Weston Nakamura and Darius Dale touched on this on “The Real Vision Daily Briefing.” Weston hits a grand slam on this analysis. He noted that Japan has two major problems right now, an energy problem and the BOJ has been working on yield curve control. The Yield curve control hasn’t hit the news much, but they’ve been buying JGBs via a fixed rate operation. With the JGB buying keeping yields down, there’s a search for yield outside of Japan, so that pushes the Yen down. Japan is really the only economy easing. Weston thinks this is coming to a head, and if Japan isn’t able to hold their line and they get overwhelmed, rates will rise. He thinks that crushes risk assets globally. While the Yen performance isn’t the worst ever, as seen in my first chart below, it is seeing a ton of pressure. The second chart is looking at the implied vol and the positioning by non-commercial traders. The title and my charts are focusing on the Yen, there’s so much on the global macro front here, I can’t recommend this session enough. What's Wrong With the Yen, and Why Is It Important? - Watch time: 37 minutes

For this week, I’ll be keeping an eye on the Yen, as noted above, but also the Fed minutes will be released. We should get a little more insight on the possibility, er probability, of a 50 bps hike in the next meeting. I’m also intrigued by what might come out of the BTIG Global Cannabis Conference. With Tilray and Constellation Brands reporting this week, we’ll get some insight on that industry. I’ll also have my eye on Bitcoin and other crypto assets. They’ve seen some positive momentum and the Bitcoin 2022 conference is in Miami.

Best of the Week

Ken Burns is one of my all time favorite documentary filmmakers. He’s in the news for his latest film out Monday April 4th on Ben Franklin. In this interview, he talks about why he chose to do this film on Franklin. If you have read the blog summary, you’ll know that the title is based on one of his papers. He’s my all-time favorite person in history. I look up to many of his qualities. Sorry, if this takes you off the path of finance, but this guy is arguably the greatest American ever. But as Burns notes, there is so much to learn from him. Some of the real value in this interview comes from Burns talking about how he works through his creations. He’s sometimes working on seven films at one time and some of them take years to finish. I mean it took me over a year to watch his Baseball film. Filmmaker Ken Burns on Lessons in Innovation and Collaboration - Listening time: 29 minutes

Best of the Rest

I was surprised to read that the percentage of global electricity generated by wind and solar was up to 10%. Fifty countries get more than that too. Clean energy as a whole generated almost 40% of the world’s electricity. The article notes that because of the increased demand some of the not clean sources like coal grew as well. Refinitiv’s Energy team tackled how the move to net zero impacts commodities. The article looks at the challenges and opportunities that face the industry. Things like supply and demand issues, pricing, and financing. Climate change: Wind and solar reach milestone as demand surges

The number of hedge fund launches in 2021 was outstanding. According to HFR, there were more than 600 new funds launched last year. That’s the most in about 5 years, when 2017 hit more than 700. Yes, there were 600 new funds, but there were also more than 500 liquidations as well. That number may seem high, but it was the lowest since 2004. HFR’s Ken Heinz said he expects funds to continue to do well in 2022. His firm estimates that the industry’s market cap now exceeds $4T. The “why” part of this according to both HFR and Pivotal Path is the worries about macro events. Hedge funds can be one of the few strategies to be able to capitalize on the esoteric events geopolitical events can create. Hedge Fund Launches Went Through the Roof Last Year — Here’s Why

Institutional Investor came to party last week. There were a few more good articles that I didn’t even include. This one focuses on the proposed rule changes coming out of the SEC that would effectively end the SPAC boom. Commissioner Hester Peirce seemed to be the only one in agreement with that statement. Chairman Gensler noted that the SEC is just trying to protect investors, and I can see that based on the recent performance of SPACs. The biggest changes are more disclosure, shortening the time to find a deal, and investors being able to sue over misleading projections. These changes will make things more costly and possibly limit much of the advantages they have over traditional IPOs. There are currently more than 500 SPACs looking for a target. SEC Deals a Big Blow to SPACs

Many people focus greatly on the “E” in ESG. This article touches on the S, for Social. Elisabetta Basilico and Tommi Johnsen asked the question, “Where are the Women?” They had as much success as someone doing a “Where’s Waldo?” book. Their research found that less than 10% of the most senior positions in financial services, CIO, Head of Research, and Head of Investment Banking, have women in them. Their research wasn’t short on sample size either with almost 10,000 positions for these positions globally. Their research looked at 29 developing countries and the 4 BRICs. The data shows that Europe leads the pack, but China’s position, at #2, in the CIO position was a surprise to me. What Percentage of Women Serve in Senior Investment Roles?

One for the Road

To wrap this week, I thought this was a great post from Ted Lamade on the Collaborative Fund site. Ted highlights that recent events should not really be unexpected. It’s sad, but true. I love his reference to Billy Joel’s ‘We Didn’t Start the Fire.’ He makes the point that since the advent of the 24/7 news cycle and rise of the internet, we’re exposed to much more extreme news. I think about my time as a kid, I had no clue what was going on in Europe. I remember a couple of really big events, but not much beyond that. Anyway, Ted makes the point that this has an impact on markets too. Markets are made of people, and people are becoming more emotional about these things. This is leading to more impulsive decision making, worsening forecasts, and increasing price of risk. Safer, Yet More Afraid Than Ever

Thanks for reading. I hope you have a stupendous week. Mine will be driven by the outcome of the NCAA Men's Basketball Championship game on Monday night.

Michael

Comments

Post a Comment